Helping you retire earlier, travel farther, and live more fully with smart money, budget cruising, healthcare abroad, and YouTube income.

Helping you retire earlier, travel farther, and live more fully with smart money, budget cruising, healthcare abroad, and YouTube income.

We’re a couple married for over 40 years, and we are showing the world that you don’t need millions to build a life full of love, travel, and freedom in retirement.

Lower costs instead of chasing a magic number.

Slow travel strategies and budget cruising.

Turn your life into content and income.

Find your monthly freedom number.

Housing, cars, and insurance.

Slow travel & cruising schedules.

Safety nets abroad.

YouTube & side projects.

A glimpse into our slow travel, budget cruising, and early retirement journey.

Coastal Archway Monument

Sightseeing Together

Ristorante Pizzeria Edén, Barcelona

Tapas & Cold Drinks

Gibraltar Port View

Exploring the Gardens

Santa Bárbara Castle, Alicante

La Sagrada Familia

Authentic Local Pizza

Streets of Spain

Statue of Juanito Villar

Sagrada Familia Architecture

Local Art & History

The Rock of Gibraltar

Classic European Alleyways

Coastal Fortress, Spain

Chocolate Tasting

Overlooking the Bay

Sunset Sail

Street Performers

Morning City Walk

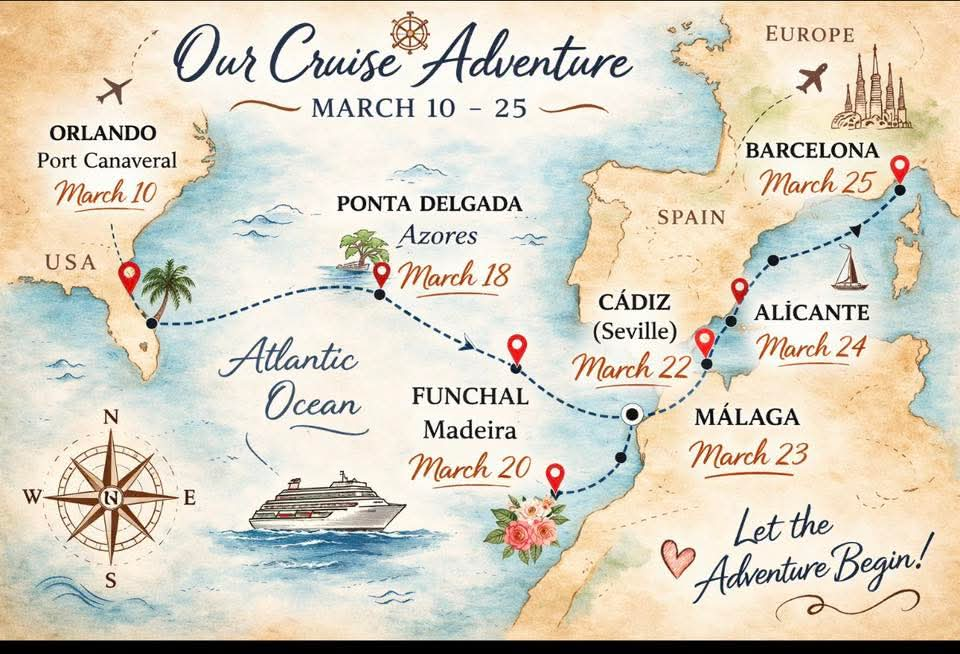

Our Route!

Focus on cash flow and lifestyle design rather than just massive accumulation.

We show you how to focus on monthly cash flow—what it really costs you to live well—so you can stop chasing random “million‑dollar” targets.

Learn how downsizing, moving to a lower‑cost area, or splitting your time abroad can slash housing costs, pulling your retirement date closer.

Before you retire, we’ll show you how you can live on your projected retirement budget for a few months so you can fix issues while you still have a paycheck.

From short getaways to months at sea, we break down cruise costs, how to find deals, and what it really takes to consider living on a cruise ship.

You’ll see real numbers, pros and cons, and how some retirees combine cruising with life on land.

Strategies for living at sea part-time.

Stay longer, spend less, experience more.

Discover how to use off‑season travel, senior discounts, and “slow travel” to turn a small travel budget into multiple trips a year.

We share sample budgets, packing lists, and step‑by-step trip plans designed specifically for retirees.

Not sure where to go? Tell us your dream, and our AI will build a custom "slow travel" itinerary perfect for the Wright lifestyle.

Designing your dream trip...

Medicare usually doesn’t cover routine care overseas. We walk you through options: local insurance, international plans, and U.S. “home base” strategies.

Read Full GuideWe highlight countries where retirees find strong hospitals and lower prices, from Mexico and Costa Rica to Portugal, Malaysia, and Thailand.

See Top LocationsUse our checklists to evaluate healthcare, visas, and costs before you choose your long‑term base or book that extended stay.

Get the ChecklistDetailed guides and strategies to help you plan your Wright Life.

Most retirees don’t need a magic “million‑dollar” number; they need a clear monthly target and a simple way to check if their savings can safely support it...

Read Article

You don't have to sacrifice safety for savings. Discover the five best countries that offer high quality of life, excellent healthcare, and low costs for 2026.

Read Article

Cruising is the ultimate way to unwind—until you find yourself confined to your cabin with a nasty virus. Here is your ultimate guide to staying healthy at sea.

Read Article

Don't pay full price for that flight to Paris. Learn how to strategically earn and redeem points to fly business class for the price of economy.

Read Article

It’s not just about lost luggage; it’s about protecting your life savings. Medicare doesn't cover you abroad—find out why medical evacuation coverage is non-negotiable.

Read Article

Gone are the days of hunting for SIM cards at the airport. Learn how digital eSIMs give you instant data in 200+ countries for a fraction of your carrier's daily rate.

Read Article

Retirement can be the beginning of your greatest adventures—not the end of them. With the right plan, you can travel more often, stay longer, and spend less...

Read Article

Healthcare is one of the biggest worries for American retirees who dream of living or traveling overseas. The good news is that many countries offer high‑quality care...

Read Article

Southeast Asia has quietly become one of the best regions in the world for retirees who want warm weather, rich culture, and low costs...

Read Article

For some retirees, cruises are an occasional treat. For others, ships become a second home—or even a full‑time address. With the right strategy...

Read Article

YouTube isn’t just for teenagers and tech experts. Retirees are quietly building channels that document their travels, share hard‑won wisdom...

Read Article

The idea of spending retirement on a cruise ship sounds like a fantasy—but for a small group of retirees, it’s real life. With careful planning...

Read ArticleWe teach you how to use your real life—early retirement, travel, cruising, and 40+ years of marriage—as content that helps others and earns you extra income.

We’re a married couple of 40+ years who decided that the “traditional” idea of retirement wasn’t enough for us. Instead of waiting for a perfect number, we focused on lowering our costs, designing a flexible lifestyle, and using creative income to fund travel and experiences.

Ready to design your own version of early retirement, travel, and freedom? Join our community for tips, stories, and tools that help you get there faster.

Cruising is the ultimate way to unwind—until you find yourself confined to your cabin with a nasty virus.

With thousands of passengers sharing dining halls, lounges, and pools, cruise ships can sometimes become hotspots for contagious illnesses like Norovirus (the dreaded "cruise bug") and COVID-19. Fortunately, staying healthy at sea is entirely possible if you play a good defense. Here is your ultimate guide to lowering your risk and knowing exactly what to do if illness strikes.

If you wake up feeling unwell in the days leading up to your departure, stay home. Do not try to power through it. Cruise lines have strict, mandatory pre-screening measures to protect the ship's ecosystem. You may be required to sign health and travel history declarations and undergo temperature checks before boarding.

If you are experiencing symptoms of COVID-19, have had contact with a diagnosed individual within the last 14 days, or receive a positive test result, you will be denied boarding. If you are dealing with a gastrointestinal bug like Norovirus, medical experts recommend waiting until you have been completely symptom-free for at least two days before returning to your regular routine or interacting with others.

| Feature | Hantavirus | Norovirus (The "Stomach Flu") | Coronavirus (COVID-19) |

|---|---|---|---|

| What it is | A family of viruses spread primarily by infected rodents. | A highly contagious, resilient virus often referred to as the "stomach flu" or the "cruise bug," though it is not related to influenza. | A highly transmissible respiratory virus responsible for the recent global pandemic, caused by the SARS-CoV-2 strain. |

| How it presents | Early symptoms include fatigue, fever, and muscle aches, which can rapidly progress to severe respiratory distress. | Causes intense gastrointestinal illness, primarily presenting as vomiting and diarrhea. Symptoms can appear after a 12-to-48-hour incubation period. | Typically presents with fever, cough, shortness of breath, fatigue, and loss of taste or smell. Can require medical isolation and intensive infection control. |

| How it spreads on cruises | Extremely rare on cruise ships. Spread by inhaling aerosolized virus from rodent urine, droppings, or saliva. | Thrives in crowded environments. It spreads via person-to-person contact, contaminated food and water, and by touching infected surfaces, where it can live for more than two weeks. It can also spread through the air if someone vomits or sneezes nearby. | Spreads primarily via airborne transmission in public spaces and through contact with contaminated high-touch surfaces like handrails and elevator buttons. |

| How to avoid getting it | Avoid contact with rodents and properly ventilate and clean areas with signs of rodent infestation. | Wash hands thoroughly for at least 20 seconds with soap and water; hand sanitizer is largely ineffective against it. Disinfect surfaces with a strong bleach solution. Swap handshakes for a "cruise tap" (touching knuckles). | Adhere to ship protocols: wear non-medical masks in public, maintain social distancing, utilize touchless hand sanitization stations, and undergo pre-screening. Disinfecting wipes can kill the virus on hard surfaces. |

Travel is one of the biggest dreams for retirees—and one of the biggest fears, because of cost. The good news is that many seniors successfully travel the world on modest budgets.

Retirement travel is most sustainable when it’s planned, not impulsive. Several planners note that many retirees devote about 5–10% of their annual retirement spending to travel, often averaging around a few thousand dollars per year, depending on income.

Your greatest advantage as a retiree is time flexibility. You can travel when flights, hotels, and tours are cheapest—often by simply avoiding peak seasons and weekends.

Some countries are beautiful but brutally expensive; others are just as unforgettable at a fraction of the price.

Travel insiders agree that cutting big-ticket items matters more than stressing over small purchases.

Slow travel—staying longer in fewer places—can transform both your budget and your stress levels.

There are discounts and programs built specifically for older travelers—you just have to ask for them and plan around them.

Many new retirees overspend on travel in their first years because they treat every trip like a once‑in‑a‑lifetime event.

Medical surprises can be the most expensive part of travel if you’re not ready.

Turn all of this into a one-page plan you can revisit every year.

High-quality care at far lower prices is possible if you understand your options.

For most Americans, traditional Medicare generally does not cover routine care outside the United States. A few Medigap and Medicare Advantage plans include limited emergency coverage while traveling, but it is not a substitute for full medical insurance.

Many popular retirement destinations offer modern hospitals, English‑speaking doctors, and lower costs due to different pricing systems and lower labor expenses.

Lists of top healthcare destinations for expats frequently mention a similar group of countries that combine quality and affordability.

Warm weather, rich culture, and low costs make this region a top choice.

In many Southeast Asian cities, retirees report comfortable lifestyles on budgets that would barely cover rent and utilities in a major U.S. metro.

Retirees often worry about healthcare, but certain Southeast Asian countries are known for strong medical tourism industries.

Basing yourself in Southeast Asia turns the region into your playground. Budget airlines and buses connect cities and countries at prices that are hard to match elsewhere.

From affordable travel style to a radical retirement housing plan.

The average cruise passenger spends a few hundred dollars per day including fare and onboard costs, but frugal retirees can pay much less by choosing carefully.

People who live mostly on cruise ships report a wide range of annual costs depending on ship type, cabin choice, and onboard habits.

What you’re really buying is a bundle: housing, food, entertainment, housekeeping, and a constantly changing view.

Document your travels, share hard‑won wisdom, and generate extra income.

YouTube rewards consistency, experience, and clear storytelling—three things many seniors have in abundance.

The most successful retirement‑age creators pick a focused niche instead of trying to cover everything.

Income usually doesn't happen overnight, but it can grow over time from multiple sources.

YouTube is powerful, but it’s not a get‑rich‑quick path. View the first 6–12 months as your “apprenticeship” phase.

Can living at sea compete with traditional retirement communities?

Most retirees don’t sign a 10‑year lease on one ship. Instead, they live at sea by stringing together back‑to‑back cruises.

Estimates vary widely, but financial analyses suggest a broad range—from very frugal retirees spending in the lower five figures per year to more comfortable lifestyles costing much more.

High‑end retirement homes can cost thousands per month, sometimes more than mid‑level cruise fares once inclusive costs are added.

You are relatively healthy, enjoy routine, structure, and are comfortable living in small spaces.

Many retirees mix several months of cruising each year with time on land.

You don’t have to guess at “how much is enough.” Use clear numbers and real spending data.

Recent data shows that retirees in the U.S. spend, on average, around $60,000 per year, or about $4,600–$5,000 per month. That’s an average, not a rule.

Build your own monthly budget. List expected retirement expenses. Then add a line item for travel (5–10% of annual spending).

The 4% rule says if you withdraw about 4% of your invested savings in the first year of retirement, your money has a high historical chance of lasting roughly 30 years.

Most retirees don’t live entirely off investments; they mix several income streams like Social Security, pensions, and part-time work.

Download our free printable checklist to calculate your exact monthly number and travel budget.

We've sent the checklist to your inbox. You can also download it right now.

Download Checklist NowYou don't have to sacrifice safety for savings.

Consistently ranked as one of the safest countries in the world, Portugal offers a mild climate, excellent healthcare, and a lower cost of living.

Known for its "Pura Vida" lifestyle, Costa Rica is a nature lover's paradise. It has a stable democracy and affordable healthcare.

The "Pensionado" program is a huge draw, offering retirees discounts on everything from utility bills to entertainment.

Offers a unique mix of modern infrastructure and traditional culture. Healthcare is world-class and very affordable.

Spain has one of the best healthcare systems in the world. Cities like Valencia and Alicante offer lower costs.

It’s not just about lost luggage; it’s about protecting your life savings. Medicare generally doesn't cover you abroad.

Many seniors don't realize that standard Medicare provides zero coverage once you leave the U.S.

If you need specialized care not available locally, medical evacuation back to the U.S. or to a major hospital can cost over $100,000.

Life happens. If you or a family member gets sick before your trip, cancellation coverage reimburses your non-refundable costs.

Gone are the days of hunting for SIM cards at the airport. Digital eSIMs are the traveler's new best friend.

An eSIM (embedded SIM) is a digital version of the physical SIM card you're used to. You don't need to swap tiny plastic chips. You simply download a data plan.

With an eSIM, you can purchase and install your data plan before you even leave home.

Most modern phones allow you to use your regular SIM for calls/texts and an eSIM for data simultaneously.

Points aren't just for free domestic flights. Used correctly, they are the secret weapon for affordable luxury travel abroad.

Experts collect "Transferable Points" (like Chase Ultimate Rewards or Amex Membership Rewards). These points can be transferred to dozens of different airlines and hotels.

The fastest way to accumulate points isn't by buying coffee; it's by opening a new card and meeting the minimum spend requirement.

Transferring points to airline partners for international business class seats is the best value.

Before you leave the U.S., ensure your primary travel card has "No Foreign Transaction Fees."

Don't assume your red, white, and blue card travels with you. Here's the reality of healthcare coverage abroad.

Original Medicare generally provides no coverage for healthcare services you get outside the 50 U.S. states and U.S. territories.

There are very limited exceptions, such as if you are in the U.S. but the nearest hospital is in Canada or Mexico.

Some Medigap plans offer foreign travel exchange coverage. However, it's not unlimited. It usually pays 80% of billed charges for emergency care and has a lifetime limit of $50,000.

High quality doesn't always mean high cost. These nations are leaders in medical tourism and expat healthcare.

Malaysia is widely considered the best value for healthcare in Asia. Most doctors speak English. Costs are often 70-80% lower than in the US.

Costa Rica operates a two-tier system: the "Caja" (universal public system) and a robust private sector.

Bangkok is a global hub for medical tourism. The quality of care is exceptional.

Portugal offers high standards of care at very reasonable prices.

For convenience, Mexico is hard to beat. Cities like Puerto Vallarta, Merida, and Mexico City have excellent hospitals.

Don't leave your health to chance. Use this checklist before you book your long-term stay.

Can you get your meds there? Some drugs common in the US are illegal or highly restricted in other countries.

Even with insurance, you often have to pay upfront and file a claim later.

Don't rely on your doctor back home faxing records. Keep a digital folder with a list of current medications and allergies.

If you have a serious allergy, carry a laminated card translated into the local language that explains it clearly.

911 doesn't work everywhere. Save the local emergency number for your destination in your phone immediately upon arrival.

Whether you're at sea or settling into a month-long stay, having the right gear makes all the difference.

Cruising requires specific items due to limited cabin space and formal nights. Top recommendations from seasoned cruisers:

For long stays in Airbnbs or apartments. The goal is to live, not just visit.